Storms can strike unexpectedly, leaving a trail of destruction in their wake. Whether it’s hurricanes, tornadoes, or severe thunderstorms, understanding storm damage is essential for effective preparation and recovery. In this post, we’ll explore common types of storm damage, how to prepare your home, and tips for recovery.

Types of Storm Damage

Wind Damage

High winds can tear off roofs, uproot trees, and send debris flying. The impact can compromise structural integrity, making it crucial to assess any damage promptly.

Water Damage

Heavy rainfall can lead to flooding, causing extensive water damage to homes. Basements are particularly vulnerable, so it’s important to have proper drainage systems in place.

Lightning Strikes

Lightning can cause fires and power surges. Homes without surge protectors or proper grounding systems are at risk.

Falling Trees and Debris

Strong winds can lead to fallen trees or branches, damaging roofs, vehicles, and power lines. Regular tree maintenance can help mitigate this risk.

When the storm clouds gather and the winds begin to howl, there's one team you can trust to stand by your side and help you weather the worst. At SERVPRO® of Allentown Central and Western Lehigh County, we understand the havoc that storms can wreak on homes and businesses. From flooding and water damage to wind and debris, storms can leave a trail of destruction in their wake. But fear not, because our team is here to help you pick up the pieces and restore your property to its former glory.

Expertise in Action: With years of experience and a commitment to excellence, SERVPRO of Allentown Central and Western Lehigh County is your trusted partner in storm damage

restoration. Our team of highly trained professionals knows exactly what it takes to mitigate the damage caused by storms and get your property back to preloss condition as quickly as possible.

Rapid Response: When disaster strikes, every minute counts. That's why we offer 24/7 emergency services, so you can count on us to be there when you need us most. Our rapid response team will arrive on-site quickly to assess the damage and begin the restoration process immediately.

Comprehensive Services: From water extraction and drying to debris removal and structural repairs, SERVPRO of Allentown Central and Western Lehigh County offers a wide range of services to address all aspects of storm damage restoration. We have the equipment, expertise, and manpower to handle even the most challenging restoration projects.

Advanced Technology: We leverage the latest technology and techniques to ensure efficient and effective restoration results. Our state-of-the-art equipment allows us to thoroughly assess the extent of the damage and implement targeted restoration solutions to minimize downtime and disruption.

Attention to Detail: At SERVPRO of Allentown Central and Western Lehigh County, we believe that no detail is too small when it comes to restoring your property. Our meticulous attention to detail ensures that every aspect of the restoration process is handled with care and precision, leaving no stone unturned in our quest to deliver exceptional results.

Customer Satisfaction: Above all else, our goal is to ensure your complete satisfaction. We understand that dealing with storm damage can be overwhelming, which is why we go above and beyond to provide compassionate customer service and support every step of the way. From initial assessment to final walkthrough, we'll be there to guide you through the restoration process and answer any questions you may have.

Conclusion: When disaster strikes, don't face it alone. Trust the experts at SERVPRO of Allentown Central and Western Lehigh County to help you navigate the storm and emerge stronger on the other side. With our unwavering commitment to excellence, cutting-edge technology, and unparalleled customer service, we'll have your property restored to its former glory in no time. Contact us today to learn more about our storm damage restoration services and how we can help you weather the worst.

Weathering the Storm: SERVPRO®'s Guide to Storm Damage Restoration

Storms can wreak havoc on homes and businesses, leaving behind a trail of destruction in their wake. From powerful winds and torrential rains to flooding and debris, the aftermath of a storm can be overwhelming. However, with the right support and expertise, recovery is possible. At SERVPRO®, we specialize in storm damage restoration, helping property owners navigate the challenges and restore their spaces to pre-storm conditions.

Assessment and Safety First: After a storm, safety should always be the top priority. Before assessing the damage, it's crucial to ensure that the property is safe to enter. Once safety is established, our team at SERVPRO conducts a thorough assessment of the damage, identifying areas of concern and developing a customized restoration plan.

Swift Response, Swift Recovery: Time is of the essence when it comes to storm damage restoration. That's why SERVPRO offers 24/7 emergency service, ensuring that help is always just a phone call away. Our rapid response team arrives on-site quickly to assess the situation, mitigate further damage, and begin the restoration process immediately.

Comprehensive Restoration Services: From water extraction and drying to debris removal and structural repairs, SERVPRO offers a comprehensive range of restoration services to address all aspects of storm damage. Our certified technicians utilize advanced equipment and proven techniques to restore your property efficiently and effectively.

Navigating the Insurance Process: Dealing with insurance companies can be complex, especially in the aftermath of a storm. At SERVPRO, we understand the challenges you may face when filing a claim. That's why our team is here to help. We work closely with insurance companies to document the damage, provide accurate estimates, and facilitate the claims process, ensuring a smooth and hassle-free experience for our customers.

Community Support and Resources: SERVPRO is more than just a restoration company – we're members of the community. When disaster strikes, we're here to lend a helping hand and support our neighbors in their time of need. In addition to our restoration services, we also offer resources and guidance to help property owners prepare for future storms and minimize the risk of damage.

Don't let storm damage derail your life. Trust the experts at SERVPRO to restore your property and provide peace of mind during the recovery process. Contact us today for all your storm damage restoration needs.

Battling the Aftermath: How to Navigate Property Damage After a Storm

As the winds howl and the skies darken, storms unleash their fury, leaving behind a trail of destruction. For homeowners and property managers, the aftermath of a storm can be overwhelming, with structural damage, flooding, and debris posing significant challenges. Amidst the chaos, one beacon of hope emerges – property damage restoration companies.

Assessing the Impact

When the storm clouds clear, the first step is to assess the extent of the damage. From fallen trees to roof leaks and shattered windows, every detail matters. At SERVPRO®, our experienced team swiftly responds to calls, conducting thorough inspections to evaluate the scope of restoration needed.

Emergency Response

With time being of the essence, our rapid emergency response team springs into action. We understand that a quick response can mitigate further damage and alleviate the stress on homeowners. Equipped with advanced tools and expertise, we prioritize safety and efficiency, securing the property and initiating the restoration process.

Restoration Expertise

From water extraction and drying techniques to structural repairs and mold remediation, our restoration specialists are trained to handle diverse challenges. We adhere to industry standards and employ cutting-edge technologies to restore your property to its pre-storm condition. Our goal is not just to fix the damage but to provide peace of mind to our clients.

Navigating Insurance Claims

Dealing with insurance claims can often add to the post-storm ordeal. Our team works closely with homeowners and insurance providers, offering comprehensive documentation and support throughout the claims process. We strive to streamline the journey, ensuring a smooth and hassle-free experience for our clients.

When facing an unfortunate thunderstorm, snow storm, hurricane, tornado, or other natural disaster, more than just the structure of your home can be affected. Furniture, clothing, antiques, and keepsakes that hold memories make a home special. Thankfully, SERVPRO® has an entire contents cleaning department, dedicated to restoring your personal items and getting them to look brand new again before they were affected

We test your contents to see which items can be restored and what is more logical for you to restore rather than replace right away. We use several different methods of professional cleaning such as dry and wet cleaning, foam cleaning, abrasive cleaning, and immersion cleaning. Throughout these methods, we are able to restore your contents to the absolute best of our ability.

We can even coordinate the restoration of your technology such as computers, laptops, phones, tablets, and televisions. Document drying services are also available in the case of important documents like birth certificates and paperwork being dried out through air drying, freezer drying, or dehumidification.

With SERVPRO® of Allentown & Western Lehigh County, you don’t have to worry about a thing as we restore everything for you, from your property to your contents and belongings. Give us a call today to talk with a member of our team about what we can do for you!

SERVPRO® of Allentown & Western Lehigh County is the number one choice in cleanup and restoration, especially when it comes to storm damage and unexpected storms. Whether it’s a hurricane, tornado, or winter storm, our team is always here to help 24/7 at any time of the day or night.

We can handle both residential and commercial storm cleanup and services to get your property back to "Like it never even happened." in no time. Our team is highly trained and we have all of the essential equipment to restore both your property and your contents. SERVPRO® has an easy insurance claims process and we work with you as much as possible.

We are faster to any sized disaster and ensure you that we work as quickly and efficiently as possible to restore your commercial business or residential property. Give us a call with any storm damage today and we will be there to help in no time!

Our company is available 24/7 to help with any storm damages. Whether it’s a thunderstorm, hurricane, or snowstorm, we got you covered and we assure you that your property will appear "Like it never even happened." in no time! We can provide services from residential flooding and storm cleanup to wind damage and wildfire cleanups as well. We can handle roof tarping, board ups, and even contents cleaning services for items that may have gotten in the crossfire.

We can restore furniture, clothing, and sentimental items that may have been damaged by excessive water, sewage, or flooding as a result of your storm damages. We can also handle commercial properties as well as residential properties, and our team works hard with their expertise to restore everything to its original condition. We can secure your property with a stress-free experience as we handle everything with your insurance company! There’s no need to worry about hassle or stress involving your insurance agent because our office staff and team is in contact with them and will give you updates throughout the duration of your project.

If your property faces unexpected storm damages, be sure to give us a call at 610-776-7774! We can take on any property or business in Lehigh County and surrounding areas.

Springtime is always exciting with flowers blooming and the sun finally shining, but there can be a lot of severe weather during this time as well. Severe weather consists of several different types of weather events, including tornadoes, thunderstorms, and floods (which includes flash floods, and urban and small stream flooding). The National Severe Storms Laboratory also classifies lightning, hail, damaging winds, and harsh winter weather under the “severe weather umbrella.”

Thunderstorms typically are the most severe weather experienced in the spring. With the collision of the warm and cool air, thunderstorms can lead to damage to the roof of your home, flooding in your basement, and even trees or outside debris damaging your home.

During this storm season, make sure to have an emergency ready plan, detailing places of shelter, methods of communication in case you are separated from family and friends, evacuation routes, and more. If you need assistance putting one together, SERVPRO can help. Make sure everyone knows where emergency supplies are located and they know how to access and turn off electricity, gas, and water in your home. Be sure to have a first-aid kit, non-perishable food and water supplies, and stay tuned into weather alerts for your area.

To best prevent your home from experiencing any damages from the harsh weather, ensure the outside of your property is prepared. Trim tree branches and place valuables in a sturdy, covered location. Clear your yard and secure loose objects, ensuring nothing can blow around and cause damage (such as bikes and grills).

Close and lock windows and doors. You may consider installing storm shutters, or nailing plywood over window frames to protect yourself and family from shattered glass.

If you experience damages that need reconstruction services, need someone to clear up all of the leftover debris from the storm, or ensure your property is sanitized and safe, contact SERVPRO immediately at 610-776-7774! We are always here to help.

Unexpected events can be a worrisome time, but having a well-thought-out plan in advance can prepare your business for a lot less stress and the capability to survive any disaster. SERVPRO’s “Emergency Ready Plan” can help give you, your customers, and even your employees a peace of mind if disaster happens to strike.

Why use our Emergency Ready Plan?

No-Cost Assessment of your Facility

We provide a no-cost assessment of your facility. We are able to provide you with great value at absolutely no cost to you

Easier Insurance Claims Process

SERVPRO is able to work with insurance companies to ensure that your experience with us is as seamless as possible. Us working with your insurance allows less stress on you after already experiencing damaging losses

Profile Document

By completing a concise profile document with critical information in the event of emergency, it can save lots of time and effort to prepare for disaster before it is too late

Getting Back Safely

Have a plan of action for everyone to return to the building safely ahead of time. For example, have routes planned out for any emergency that could occur and make sure employees in the building are up to date on any procedures they need to be familiar with

Establish SERVPRO as your Provider

By connecting with a local SERVPRO to your business before disaster strikes and making them aware that you want to use their services in case of emergency, it can be easier for everyone to know exactly who to call when disaster strikes

Line of Command

Save time and money by allowing SERVPRO to work with any mitigation damages and authorize our company to take care of your problems

Facility Emergency Details

Provide us with facility details such as shut-off valve locations, priority areas and priority contact information. Being ready for whatever can happen will save you time and stress during the actual emergency. Having contact numbers and electrical locations to shut off in case of emergency can allow employees to know exactly what to do

After a harsh storm your home or commercial property can be left with a lot of water damage. Water can damage materials inside your home and leave behind a lot of problems that need to be fixed. That’s where we come in! Wallboards can begin to disintegrate if they remain wet for too long; floorboards can warp, sell or rot; and electrical circuits can short out or malfunction resulting in fire damages as well. Dampness can also promote mildew growth which can lead to health concerns. Our production team undergoes extensive training, including Institute of Inspection Cleaning and Restoration Certification (IICRC) Certified. At SERVPRO of Allentown & Western Lehigh County we are here for you in case of any emergency.

If you notice any of these issues arise in your home after a storm call SERVPRO of Allentown & Western Lehigh County at 610-776-7774, we offer 24/7 emergency services and will be there day or night to help you and your family!

We all watch the news and hear of hurricane season affecting coastal states. What most people don’t realize is that hurricane season can also affect inland states and cause damage to homes and businesses. Check out some of these hurricane season myths and truths to keep you safe this hurricane season:

Myth: Only homes and communities on the coast need to be worried when a hurricane is approaching. People living further inland are safe.

Truth: Some hurricanes can create winds that have a 1000 mile diameter. These winds can also spawn other destructive weather such as tornadoes that can reach hundreds of miles inland.

Myth: Flooding only happens in a coastal area.

Truth: Storm surges from hurricanes can travel tens of miles inland. Rain from hurricanes can cause flooding hundreds of miles away from the coastline.

Myth: My home and homeowners insurance policy will cover all damages from a hurricane.

Truth: Standard property insurance policies, like home or homeowners insurance, provide protection from many things, including some of the damages caused by a hurricane. They will not, however, cover flood damage, whether it comes from the storm surge or rainfall.

While we won’t get hit with the brunt of a hurricane we can be susceptible to property damages caused by one. Stay alert during this season and monitor your local weather. SERVPRO of Allentown & Western Lehigh County offers 24/7 emergency services. Give us a call if your home or business becomes damaged this hurricane season, 610-776-7774!

After a harsh storm your home or commercial property can be left with a lot of water damage. Water can damage materials inside your home and leave behind a lot of problems that need to be fixed. That’s where we come in! Wallboards can begin to disintegrate if they remain wet for too long; floorboards can warp, sell or rot; and electrical circuits can short out or malfunction resulting in fire damages as well. Dampness can also promote mildew growth which can lead to health concerns. Our production team undergoes extensive training, including Institute of Inspection Cleaning and Restoration Certification (IICRC) Certified. At SERVPRO of Allentown & Western Lehigh County we are here for you in case of any emergency. If you notice any of these issues arise in your home after a storm call SERVPRO of Allentown & Western Lehigh County at 610-776-7774, we offer 24/7 emergency services and will be there day or night to help you and your family!

Do You Have Storm Damage? Call SERVPRO of Allentown and Western Lehigh County!

A storm can cause damage to your house or business. When damage occurs you need to take action quickly. You may feel stressed after your property was affected by a storm. However, it needs to be handled fast and effectively. At SERVPRO of Allentown and Western Lehigh County we try to lessen your stress of dealing with storm damage by making your claims stress free and help to manage the insurance process and paperwork.

You cannot always plan for when disasters will strike, but you can be prepared for what to do after your home or business has been affected by storm damage. At SERVPRO of Allentown and Western Lehigh County we want you to know that we have years of experience in cleaning up messes that a storm can leave behind. Whether your house is flooded from heavy rains or there's a hole in your businesses’ roof from a tree falling down, we have the equipment and expert manpower for the job.

Do you have storm damage to your residential or commercial property? Call SERVPRO of Allentown and Western Lehigh 24/7 at 610-776-7774!

This week is National Hurricane Preparedness Week. Hurricane season is around the corner, starting on June 1st.

The first tip is to check your county website to find out if your home is in an evacuation zone. Next, check your county’s website to determine if your property is a flood risk. To do so, you can use FEMA’s Flood Map Service at no charge. This tool will use your property address to identify a flood zone.

In the event of a flood prepare an emergency supply kit. In this kit, you should have nonperishable food, water and medicine.

Did you know that homeowner insurance does not cover floods. Flood insurance is a separate plan and should be added onto your homeowners insurance plan.

If a flood occurs, call the storm damage experts, SERVPRO of Allentown and Western Lehigh County today - 610-776-7774!

After a harsh storm a lot of damage can occur due to water. At SERVPRO of Allentown and Western Lehigh County we are here to help you understand. The water damages materials. Wallboard will disintegrate if it remains wet too long; wood can swell, warp, or rot; electrical parts can short out, malfunction, and cause fires or shock.

Mud, silt and unknown contaminants in the water not only get everything dirty, they also create a health hazard.

Dampness promotes the growth of mildew, a mold or fungus that can grow on everything.

The following steps work on all three of these problems. It is very important that they be followed in order.

Lower the humidity: Everything will dry more quickly and clean more easily if you can reduce the humidity in the home. There are five ways for you to lower the humidity and stop the rot and mildew. But you'll have to delay using some methods if you have no electricity.

Open up the house: If the humidity outside is lower than indoors, and if the weather permits, open all the doors and windows to exchange the moist indoor air for drier outdoor air. Your body will tell if the humidity is lower outdoors. If the sun is out, it should be drier outside. If you have a thermometer with a humidity gauge, you can monitor the indoor and outdoor humidity.

On the other hand, when temperatures drop at night, an open home is warmer and will draw moisture indoors. At night and other times when the humidity is higher outdoors, close up the house.

Open closet and cabinet doors: Remove drawers to allow air circulation. Drawers may stick because of swelling. Don't try to force them. Speed drying by opening up the back of the cabinet to let the air circulate. You will probably be able to remove the drawers as the cabinet dries out.

Use fans: Fans help move the air and dry out your home. Do not use central air conditioning or the furnace blower if the ducts were under water. They will blow out dirty air, that might contain contaminants from the sediment left in the duct work. Clean or hose out the ducts first.

Run dehumidifiers: Dehumidifiers and window air conditioners will reduce the moisture, especially in closed up areas.

SERVPRO of Western Lehigh County specializes in storm and flood damage restoration. We have highly trained staff and specialized equipment to restore your property! We have 24 hour emergency service.

Faster to any disaster:

Since we are locally owned and operated, we are able to respond quicker with the right resources, which is extremely important. A fast response lessens the damage, limits further damage, and reduces the restoration cost.

Storms:

When storms hit Lehigh County, we can scale our resources to handle a large storm or flooding disaster. We can access equipment and personnel from a network of 1,700 Franchises across the country and elite Disaster Recovery Teams that are strategically located throughout the United States.

We can help you with your storm damage! Call SERVPRO of Western Lehigh County at 610-776-7774!

Storm damage can strike your commercial property at any time. Water damage can sideline your business, regardless of if the damage occurs from a major storm event or a broken water line. Every hour spent cleaning up is an hour of lost revenue and productivity. So when you have an emergency water event, SERVPRO of Allentown Central and Western Lehigh County Franchise Professionals offer fast, 24 hour emergency services, 365 days per year.

Here are some tips:

Remove excess water by mopping and blotting.

Wipe excess water from wood furniture after removal of lamps and tabletop items.

Remove and prop wet upholstery and cushions.

Place aluminum foil or wood blocks between furniture legs and wet carpeting.

Turn air conditioning on for maximum drying in summer.

When you think of storms you might think of rain, however strong winds can easily knock down power lines and cause fires that can destroy homes and make life difficult. You cant always plan for when disasters will strike, but you can be prepared for what to do after your home or business has been affected by storm damage. At SERVPRO of Carbon County we want you to know that we have years of experience in cleaning up messes that a storm can leave behind. Whether your house is flooded from heavy rains or there's a hole in your roof from a tree falling down we have the equipment and expert man power for the job. We can handle all of your problems and needs quickly and thoroughly to ensure that your normal life whether at home or at your business is back up and running.

As we experienced flooding in the past couple of weeks, you might have flooding in your home. It is important to call the professionals at SERVPRO of Allentown and Western Lehigh County to properly clean up your property. In the meantime, here are some tips to keep in mind when flooding occurs in your home.

If you are using a generator, always leave it outside of the home. As you may know, generators use gases that can be extremely dangerous to expose yourself or your family to. In addition, you do not want to leave a generator outside of an open window, as the fumes can still come into the home.

After a flood, your drinking well water may have been contaminated with waterborne pathogens. Do not drink or cook with this water if it is contaminated.

SERVPRO of Western Lehigh County is here for you, your loved ones and your home. We know storms can be devastating and leave you with nothing. We want to take the time to share some information about what to do when you are experiencing a storm.

What to Do After a Hurricane

Find your loved ones. ...

Don't go home until it's safe. ...

Document the damage. ...

Contact your insurance company. ...

Apply for assistance. ...

Stay out of the water. ...

Prevent further damage. ...

Listen to local clean up news and advisories.

Standard homeowners policies cover wind damage. So, if hurricane winds or tornadoes wreck your home, you should be OK. However, if a storm surge or flood carries off your house, a standard policy won't make you whole. You'll still have a mortgage if your house is destroyed by flooding.

Fill your bathtub with water, unless you have little children. This water can be used for drinking, washing, and flushing the toilet. Water supplies are often compromised by hurricanes and either become undrinkable or stop flowing.

Stay Safe After a Hurricane or Other Tropical Storm

Stay out of floodwater.

Never use a wet electrical device.

If the power is out, use flashlights instead of candles.

Prevent carbon monoxide poisoning.

Be careful near damaged buildings.

Stay away from power lines.

Protect yourself from animals and pests.

Drink safe water. Eat safe food.

If you have no flood insurance, FEMA's IHP grant will help you in a specific set of ways after a flood or other disaster. ... This is much less coverage than NFIP flood insurance, which covers up to $250,000 to repair or replace your home and belongings.

Once the storm clears, call SERVPRO of Western Lehigh County to help you!

SERVPRO of Western Lehigh County specializes in storm and flood damage restoration. We have highly trained staff and specialized equipment to restore your property! We have 24 hour emergency service.

Faster to any disaster:

Since we are locally owned and operated, we are able to respond quicker with the right resources, which is extremely important. A fast response lessens the damage, limits further damage, and reduces the restoration cost.

Storms:

When storms hit Lehigh County, we can scale our resources to handle a large storm or flooding disaster. We can access equipment and personnel from a network of 1,700 Franchises across the country and elite Disaster Recovery Teams that are strategically located throughout the United States.

We can help you with your storm damage! Call SERVPRO of Western Lehigh County at 610-776-7774!

Storms occur and we will be able to respond quickly to any disaster! We specialize in flooding and storm damage restoration, the cornerstone of our business. We have extensive water damage and storm restoration training that allows us to get your home back to normal quickly.

At SERVPRO of Western Lehigh County, we can restore storm and flood-damaged properties. Our highly trained professionals have the skills and expertise to restore your home or business. We can mitigate, remediate, abate, cleanup, and reconstruction services.

Locally owned company with National Storm resources:

SERVPRO of Western Lehigh County is locally owned and operated, so we are part of this community too. When you have a flooding or storm emergency, we’re already nearby and ready to help. We take pride in being a part of the Emmaus community and want to do our part in making it the best it can be.

We are proud to serve our local communities: Emmaus, Macungie, Fogelsville, Zionsville, Coopersburg, Center Valley, Alburtis, Breingsville and Trexlertown.

Storm Damage? SERVPRO of Western Lehigh County can help!

A storm can cause damage to your house or business. When damage occurs you need to take action quickly. You may feel stressed after your property was affected by a storm. However, it needs to be handled fast and effectively. First, check how much damage is done. It is important to check every inch of your property to ensure proper repairs are made.

Safety first! When you are checking the damage you should avoid electrical equipment. If you observe any cracks on the roof, do not stand under or close to the affected area.

Contact your insurance! As you are in the house, you will want to take pictures as proof of damage for your insurance company. In addition, they will most likely send an insurance adjuster to your property to examine the damage.

You will want to call professionals in to clean and restore your home. Who are you going to call? SERVPRO of Western Lehigh County! Why SERVPRO? You should call us because we are faster to any size disaster and offer 24-hour emergency service!

Call SERVPRO of Western Lehigh County at 610-776-7774!

The SERVPRO Commercial Large Loss Division is composed of our best of the best in restoration. Our elite large-loss specialists are prequalified and strategically positioned throughout the United States to handle any size disaster.

At SERVPRO, the difference is our ability to dispatch trained production professionals and cut costs through the strategic placement and oversight of temporary labor.

Sourced from www.Everydayhealth.com, below are 4 things to do before a disaster strikes:

1. Learn Evacuation routes: Be sure to contact your local officials and find out how you should get out of your area if you need to.

2. Have a family emergency plan: it down and talk about the emergencies that are most likely to happen in your area. Determine how your family will react in each situation.

3. Assemble an emergency kit: In a tote or other easy-to-carry bag, store copies of important documents such as birth certificates, photo identification, medical cards, cash and extra checks, spare keys, an extra supply of prescription medications, a three-day supply of water and non-perishable food (don't forget pet food), a first-aide kit a flashlight, matches, blankets, and changes of clothing.

4.Keep your gas tank filled: Since you will likely need your automobile to evacuate your area, it is a good rule of thumb to always refill your gas tank when it dips below half.

Cold weather can have a huge impact on your home or business if you are not prepared. Whether it is heavy rain, freezing temperatures, damaging winds, sleet or snow all can cause serious property damage. While you can't control the weather, you can take steps to be prepared, and help take the sting out of winter weather. Check your property for downed tree limbs and branches. Weather, such as wind, heavy rain, ice and snow can cause damage to the property and potentially cause personal injury. Inspect property, especially walkways and parking lots for proper drainage to alleviate flood hazard potential. Ask SERVPRO of Western Lehigh County about completing an Emergency Ready Profile (ERP) for your business. The ERP is a no cost assessment to your facility, and provides you with a plan to get back in business fast following a disaster.

Here at SERVPRO of Western Lehigh County we care about the safety of you and your loved ones and your home. Storms can be devastating and leave you with nothing. We want to educate you on some popular questions people ask when a storm of any kind comes through a home.

What to Do After a Hurricane

Find your loved ones. ...

Don't go home until it's safe. ...

Document the damage. ...

Contact your insurance company. ...

Apply for assistance. ...

Stay out of the water. ...

Prevent further damage. ...

Listen to local clean up news and advisories.

Standard homeowners policies cover wind damage. So, if hurricane winds or tornadoes wreck your home, you should be OK. However, if a storm surge or flood carries off your house, a standard policy won't make you whole. You'll still have a mortgage if your house is destroyed by flooding.

Fill your bathtub with water, unless you have little children. This water can be used for drinking, washing, and flushing the toilet. Water supplies are often compromised by hurricanes and either become undrinkable or stop flowing.

Stay Safe After a Hurricane or Other Tropical Storm

Stay out of floodwater.

Never use a wet electrical device.

If the power is out, use flashlights instead of candles.

Prevent carbon monoxide poisoning.

Be careful near damaged buildings.

Stay away from power lines.

Protect yourself from animals and pests.

Drink safe water. Eat safe food.

If you have no flood insurance, FEMA's IHP grant will help you in a specific set of ways after a flood or other disaster. ... This is much less coverage than NFIP flood insurance, which covers up to $250,000 to repair or replace your home and belongings.

Most important after you know your family is safe, call SERVPRO to help you get your life back together.

Storm damages can be very scary and can take a while to recover from. SERVPRO of Western Lehigh County has done quite a few clean ups after some storm damages. Here are some good things to learn about storms.

According to the National Severe Storms Laboratory, thunderstorms can cause damage due to high winds, flash flooding from rain and from lightning strikes. Strong thunderstorms can also spawn tornadoes, which can cause massive destruction to personal and business property.

According to the National Severe Storms Laboratory, thunderstorms can cause damage due to high winds, flash flooding from rain and from lightning strikes. Strong thunderstorms can also spawn tornadoes, which can cause massive destruction to personal and business property.

After a hurricane hits a coastal area, it can travel inland. At this point, the storm has typically weakened, but it can still cause damage. Torrential rains from the storm can cause rivers to flood their banks and mudslides to form. Around the world, about 10,000 people die each year in hurricanes and tropical storms.

Homeowners insurance may help cover certain causes of storm damage, including wind, hail and lightning. However, damage caused by flood and earthquakes typically is not covered by a standard homeowners insurance policy.

Storms have the potential to harm lives and property via storm surge, heavy rain or snow causing flooding or road impassibility, lightning, wildfires, and vertical wind shear. Systems with significant rainfall and duration help alleviate drought in places they move through.

Storm damages can be very scary and can take a while to recover from. SERVPRO of Western Lehigh County has done quite a few clean ups after some storm damages. Here are some good things to learn about storms.

According to the National Severe Storms Laboratory, thunderstorms can cause damage due to high winds, flash flooding from rain and from lightning strikes. Strong thunderstorms can also spawn tornadoes, which can cause massive destruction to personal and business property.

According to the National Severe Storms Laboratory, thunderstorms can cause damage due to high winds, flash flooding from rain and from lightning strikes. Strong thunderstorms can also spawn tornadoes, which can cause massive destruction to personal and business property.

After a hurricane hits a coastal area, it can travel inland. At this point, the storm has typically weakened, but it can still cause damage. Torrential rains from the storm can cause rivers to flood their banks and mudslides to form. Around the world, about 10,000 people die each year in hurricanes and tropical storms.

Homeowners insurance may help cover certain causes of storm damage, including wind, hail and lightning. However, damage caused by flood and earthquakes typically is not covered by a standard homeowners insurance policy.

Storms have the potential to harm lives and property via storm surge, heavy rain or snow causing flooding or road impassibility, lightning, wildfires, and vertical wind shear. Systems with significant rainfall and duration help alleviate drought in places they move through.

After a harsh storm a lot of damage can occur due to water. At SERVPRO of Western Lehigh County we are here to help you understand. The water damages materials. Wallboard will disintegrate if it remains wet too long; wood can swell, warp, or rot; electrical parts can short out, malfunction, and cause fires or shock.

Mud, silt and unknown contaminants in the water not only get everything dirty, they also create a health hazard.

Dampness promotes the growth of mildew, a mold or fungus that can grow on everything.

The following steps work on all three of these problems. It is very important that they be followed in order.

Lower the humidity: Everything will dry more quickly and clean more easily if you can reduce the humidity in the home. There are five ways for you to lower the humidity and stop the rot and mildew. But you'll have to delay using some methods if you have no electricity.

Open up the house: If the humidity outside is lower than indoors, and if the weather permits, open all the doors and windows to exchange the moist indoor air for drier outdoor air. Your body will tell if the humidity is lower outdoors. If the sun is out, it should be drier outside. If you have a thermometer with a humidity gauge, you can monitor the indoor and outdoor humidity.

On the other hand, when temperatures drop at night, an open home is warmer and will draw moisture indoors. At night and other times when the humidity is higher outdoors, close up the house.

Open closet and cabinet doors: Remove drawers to allow air circulation. Drawers may stick because of swelling. Don't try to force them. Speed drying by opening up the back of the cabinet to let the air circulate. You will probably be able to remove the drawers as the cabinet dries out.

Use fans: Fans help move the air and dry out your home. Do not use central air conditioning or the furnace blower if the ducts were under water. They will blow out dirty air, that might contain contaminants from the sediment left in the duct work. Clean or hose out the ducts first.

Run dehumidifiers: Dehumidifiers and window air conditioners will reduce the moisture, especially in closed up areas.

As it turns out you dont need rain for a storm to be dangerous. Strong winds can easily knock down power lines and cause fires that can destroy homes and make life difficult. You cant always plan for when disasters will strike, but you can be prepared for what to do after your home or business has been affected by storm damage. At SERVPRO of Western Lehigh County we want you to know that we have years of experience in cleaning up messes that a storm can leave behind. Whether your house is flooded from heavy rains or there's a hole in your roof from a tree falling down we have the equipment and expert man power for the job. We can handle all of your problems and needs quickly and thoroughly to ensure that your normal life whether at home or at your business is back up and running.

As the summer season comes to a close we at SERVPRO of Western Lehigh County want to remind you that the summer season of heavy winds and rain can take a toll on your roof and can cause problems not too far down the road. When storm season is said and done your roof can be left with missing shingles and wore down areas that can lead to leaking and potential structural damage when snow season arrives. Leaky roofs can damage property and cause your bills to rise if heating or air conditioning escapes through the holes in your roof from a rough storm season. It can also lead to disastrous cave-ins if there is a rough snow season, when snow piles up on your roof it can be heavy amounts of weight on your roof. When a roof isn't structured enough it can lead to cave ins and potential damage to everything in your top floor of your house. At SERVPRO of Western Lehigh County we want you to be safe and be smart by keeping up with the wear and tear of your roof during storm season and to know who to call when problems arise

When storms happen in the northeast part of our area, it is always some kind aftermath of the storm. Whether its down tree branches and power lines. The aftermath damages from a storm from the wind or hail to home or business. Flooding from the rain, in and around the buildings or homes. Power outages or other utility outages. It is a mess that no one wants to tell with, but you can always count on the professional of SERVPRO of Western Lehigh County to regain some peace of mind and to return to normal with our clean up services to the community both residential and commercials. We are here to service your day or night from that aftermath of any storm that comes to the Allentown area.

We are in the middle of hurricane season. Right here in the United States, September is recognized as National Preparedness Month which serves as a reminder that we all must take action to prepare, now and throughout the year for the types of emergencies that could affect us where we live, work and visit. Did you know SERVPRO of Western Lehigh County offers a FREE emergency ready profile that anyone can set up using a smartphone or tablet? SERVPRO of Western Lehigh County has ensured making your emergency ready plan is available at the touch of your fingertips through our FREE app available in your app store. Of course, in the spirit of being prepared and ready for any disaster that could happen, we hope everyone adds SERVPRO of Western Lehigh County to your contingency plans both at work and home. Protecting your home by knowing our services are available 24 hours a day, 365 days each year is a great way to stay prepared.

Knowing all types of storms and the destruction they can cause!

Severe weather can happen any time, anywhere. Being prepared to act quickly can be critical to staying safe during a weather event. in 2018, there were seven weather and climate disaster events across the United States. These events included five severe weather tornado events, a major floor event, and the western drought heat wave. Overall, these events killed 353 people and had significant economic effects on the areas impacted. Knowing your risk of severe weather, taking action and being an example are just a few steps you can take to be better prepared to save your life and assist in saving the lives of others. You can never predict when a large storm may hit, or the destruction it could bring. Knowing that SERVPRO of Western Lehigh County will be one of the first to respond to help in disaster cleanup is always good to know. We are trained for these type of terrible situations!

SERVPRO of Western Lehigh County has dealt with our fair share of storms over the years. We all know how devastating something such as a hurricane can be especially when you may live by the water. Flooding and then mold occur and can completely ruin your home, building, or business. SERVPRO of Western Lehigh County takes pride in how we come together across the country to help those in need. We have traveled far and wide for the largest of damages. We understand how important it is to get your life back together so with all the franchises across the country we band together to get towns, cities, states back up and running. With our tractor trailers of equipment and vehicles filled with employees ready to repair everything as soon as possible. We understand your property hold value to you in more ways than one and we want you to have that comfort knowing we care and we go the extra mile to handle a disaster recovery. Just know that you can call SERVPRO of Western Lehigh County for any job no matter how big or how small. We can handle it!

When Storms or Floods hit Lehigh County, SERVPRO is ready!

Our highly trained crews are ready to respond 24/7 to storm or flood damage in Lehigh County.

SERVPRO of Western Lehigh County specializes in storm and flood damage restoration. Our crews are highly trained and we use specialized equipment to restore your property to its pre-storm condition.

Faster Response

Since we are locally owned and operated, we are able to respond quicker with the right resources, which is extremely important. A fast response lessens the damage, limits further damage, and reduces the restoration cost.

Resources to Handle Floods and Storms

When storms hit Lehigh County, we can scale our resources to handle a large storm or flooding disaster. We can access equipment and personnel from a network of 1,650 Franchises across the country and elite Disaster Recovery Teams that are strategically located throughout the United States.

Have Storm or Flood Damage? Call Us Today 610.776.7774

National Preparedness Month: National Flood Insurance

The National Flood Insurance Program aims to reduce the impact of flooding on private and public structures.

The National Flood Insurance Program aims to reduce the impact of flooding on private and public structures. It does so by providing affordable insurance to property owners, renters and businesses and by encouraging communities to adopt and enforce floodplain management regulations. These efforts help mitigate the effects of flooding on new and improved structures. Overall, the program reduces the socio-economic impact of disasters by promoting the purchase and retention of general risk insurance, but also of flood insurance, specifically.

This year (2018) the NFIP celebrates 50 years of protecting people in the United States against the perils of flood damage.

HURRICANES HARVEY AND IRMA NOTE: If you've been impacted by Hurricane Harvey, this page provides resources about how to File Your Flood Claim.

I Don't Have Flood Insurance--Why Do I Need It?

Use our interactive tool to find out how much a flood could cost you, and watch this short but informative video to learn more about the value of having flood insurance, Why do I Need to Rethink Insurance?

FACT: Floods are the nation’s most common and costly natural disaster and cause millions of dollars in damage every year.

FACT: Homeowners and renters insurance does not typically cover flood damage.

FACT: Floods can happen anywhere--More than 20 percent of flood claims come from properties outside the high risk flood zone. Check out The Big Cost of Flooding.

FACT: Most federal disaster assistance comes in the form of low-interest disaster loans from U.S. Small Business Administration (SBA) and you have to pay them back. FEMA offers disaster grants that don't need to be paid back, but this amount is often much less than what is needed to recover. A claim against your flood insurance policy could and often does, provide more funds for recovery than those you could qualify for from FEMA or the SBA--and you don't have to pay it back.

FACT:You may be required to have flood insurance. Congress has mandated federally regulated or insured lenders to require flood insurance on mortgaged properties that are located in areas at high risk of flooding. But even if your property is not in a high risk flood area, your mortgage lender may still require you to have flood insurance.

Flood insurance helps more: Check out your state's flood history with FEMA's interactive data visualization tool. Roll your cursor over each county to see how many flooding events have happened. The tool allows you to compare how much FEMA and the U.S. Small Business Administration have provided in terms of federal disaster aid after Presidential Disaster Declarations to the amount the National Flood Insurance program has paid to its policyholders. It's easy to see that having flood insurance provides a lot more help for recovery.

I Have Flood Insurance--Do I Really Need To Keep It?

You realize your flood insurance policy is about to expire and you’re on the fence about renewing: It hasn’t flooded in your area in years (or ever). And you really could use that extra money to buy something you really want. Watch this short, informative video, Why Do I Need to Rethink Insurance?

But wait!

DON’T. RISK. IT.

FACT: Flooding is the most common natural disaster in the United States, affecting every region and state, including yours.

FACT: Flood insurance can be the difference between recovering and being financially devastated.

FACT: The damage from just one inch of water can cost more than $20,000. Check out The Big Cost of Flooding.

FACT:You may be required to have flood insurance. Congress has mandated federally regulated or insured lenders to require flood insurance on mortgaged properties that are located in areas at high risk of flooding. But even if your property is not in a high-risk flood area, your mortgage lender may still require you to have flood insurance.

FACT: If you allow your flood insurance policy to lapse for either more than 90 days, or twice for any number of days, you may be required to provide an Elevation Certificate (if you don't have one), and you may no longer be eligible for policy rate discounts you might have been receiving prior to the policy lapse. It's important to talk with your insurance agent before canceling or not renewing the policy.

FACT: Flood damage is not typically covered by homeowners insurance.

FACT: No home is completely safe from potential flooding devastation—why risk it?

FACT: If you live in a high risk flood zone, and you've received federal disaster assistance in the form of grants from FEMA or low-interest disaster loans from the U.S. Small Business Administration (SBA) following a Presidential Disaster Declaration, you must maintain flood insurance in order to be considered for any future federal disaster aid.

FACT: Storms are not the only cause of floods. Flooding can be caused by dams or levees breaking, new development changing how water flows above and below ground, snowmelt and much more.

FACT: Too often, Americans are caught off guard by the emotional and financial costs of flood damage.

Flood insurance helps more: Check out your state's flood history with FEMA's interactive data Visualization Tool. Roll your cursor over each county to see how many flooding events have happened. The tool allows you to compare how much FEMA has provided in terms of federal disaster aid (through its Individuals & Households Program) after Presidential Disaster Declarations to the amount the National Flood Insurance Program has paid to its policyholders. It's easy to see having flood insurance provides a lot more help for recovery.

To renew your policy, call your flood insurance agent. If you don’t have your insurance agent’s contact information, call the National Flood Insurance Program’s Help Center at 1-800-427-4661.

Who Can Buy Flood Insurance?

If you are a renter or homeowner (residential policy); or business owner (non-residential policy) and your property is located in a NFIP-participating community, you can purchase a policy. Contact your insurance agent to find out if your community participates in the National Flood Insurance Program.

Flood insurance from the NFIP is only available in participating communities. Ask your agent if your state and community participate, or look it up online in the Community Status Book.

Find an insurance agent near you. The agent who helps you with your homeowners or renters insurance may be able to help you with purchasing flood insurance too.

You can only purchase flood insurance through an insurance agent; you cannot buy it directly from the National Flood Insurance Program (NFIP). If your insurance agent does not sell flood insurance, you can:

Contact the National Flood Insurance Program’s Help Center at 1-800-427-4661 to request an agent referral.

How Do I Renew, Change Or Pay For My Flood Insurance Policy?

Your flood insurance agent can help you make changes to, pay for, or renew your flood policy. If your lender requires you to have flood insurance, contact them directly to ask questions about renewing or changing your policy. Your payments could be included in financial transactions associated with your mortgage.

My Question Is About Flood Maps--What Should I Do?

Find out if your community has a recent or upcoming flood map change. When your community’s flood map is updated to reflect the current risks where you live, requirements for flood insurance coverage and the costs of your policy can also change.

Community and state leaders, insurance industry professionals, as well as policyholders, renters, homeowners and businesses will find its resources helpful. We have organized this guide to provide succinct information in an easy-to-navigate document and included important, key contact information. To ensure it can be updated as the program evolves, this document has been published electronically.

Read about everything from mitigating your home to reduce flood damage, to information about weather alerts and how to stay safe when it's flooding in, How to Prepare for a Flood.

Flood claim appeals and guidance (please note--you cannot appeal a claim until you receive a denial [for some or all of your claim amount] from your insurance company.)

What Can I Do To Prepare For Or Even Reduce Flood Damage? And Can Doing These Things Lessen How Much I Pay For Flood Insurance?

What you pay for flood insurance has a lot to do with how much flood risk is associated with your building. It makes sense to reduce flood risk no matter what, but in some instances reducing flood risk can also lead to lower flood insurance costs. Below are some resources to help, but discussing your policy options with your insurance agent is the best place to start.

Communities enrolled in the NFIP's Community Rating System can get discounts on their flood insurance, learn more here.

The Homeowner's Guide to Retrofitting can help you decide the right method to mitigate future damage and loss by considering various factors, such as hazards to your home, permit requirements, technical limitations, and costs. This guide also helps you develop a flood protection strategy.

The Increased Cost of Compliance (ICC) coverage, for eligible properties that are required to be in compliance with local floodplain requirements, can help pay for elevating a building after a flood. Another way to get help with the cost of elevating your building would be through one of FEMA's various grant programs. The grants are administered by states, and each state decides which projects it will fund and for how much. Contact your local floodplain manager for more information.

Did you know? An elevated home, like the one shown on the 5 Ways to Lower Your Flood Insurance Premium, with a first floor elevated 3 feet above the base flood elevation, can expect to save 60 percent or more on annual flood insurance premiums.

Did you know? Elevating just one foot above the Base Flood Elevation often results in a 30% reduction in annual premiums.

Source: Ready.gov

National Preparedness Month: How to file a flood claim

Collect all documents and protect them in a safe place in case of a flood!

How Do I File My Flood Claim?

It can be a very overwhelming time for a property owner or renter following a flood. The information below will provide you with what you need to know about filing a flood insurance claim, tips on what you can do and need to know before your flood insurance adjuster visits your property and the other visitors you can expect at your property. The more you know, the smoother the process will go.

You should report your loss immediately to your insurance agent or insurance carrier and ask them about Advance Payments.

Find your insurer on this list of insurance companies administering National Flood Insurance Program (NFIP) flood insurance and report your claim right away. If you need assistance finding your insurance carrier, please call 800-427-4661. Help is available in most languages. Individuals who are deaf or hard-of-hearing can use TTY 800-462-7585.

If you have a policy written directly with the NFIP (i.e., your Declaration Page has the FEMA logo in the top corner), it's fast and easy to report your claim directly to the NFIP's Direct Servicing Agent.

You should have the following information available when reporting your claim:

Policy Declarations page (official document detailing your flood insurance coverage), if available

How you can be reached: telephone number or alternate contact number and email address

The insured property location

The name of any mortgage company(s)

A claims adjuster should contact you within 24-48 hours, but it may take longer, depending on the severity of the flood event.

NOTE: Your NFIP policy does not cover Additional Living Expenses, including temporary housing, but if you qualify, FEMA’s Individuals and Households Program might be able to help. So, it’s important to register for assistance with FEMA, even if you have flood insurance.

Registering online, at DisasterAssistance.gov is the quickest way to register for FEMA assistance. If you do not have access to the internet, you may register by calling 800-621-3362 or TTY 800-462-7585. If you use 711 relay or Video Relay Service (VRS), call 800-621-3362 directly. The toll-free telephone numbers will operate from 6:00 a.m. to 10:00 p.m. (local time) seven days a week until further notice.

Before entering a flooded building, make sure it’s safe.

Take as many photos and/or videos of your flood-damaged property as you can, both on the outside and the inside of the building, and label them, by room, before you remove anything—including items of exceptional value. For items like washers and dryers, hot water heaters, kitchen appliances, televisions and computers, make sure you take a photograph of the make, model and serial number. This information should be provided to your adjuster.

Remove your flood damaged items:

For your building items (e.g., flooring), retain samples such as carpet, wallpaper and drapes for your adjuster’s inspection.

For your personal property items, separate the damaged from undamaged items for your adjuster’s inspection.

Immediately throw away flooded items that pose a health risk, such as perishable food, clothing, cushions and pillows, after photographing them.

Confirm your available NFIP coverage. Some policyholders may only have building or contents (personal property items) coverage, not both.

Contact repair services if the building’s electrical, water or HVAC systems are damaged. It’s important to consult your adjuster or insurance carrier before you sign any agreement/contract with a cleaning, remediation or maintenance contractor.

Contact your community building department and floodplain administrator to get the following information:

Whether your property was substantially damaged;

Tips on how to better protect or repair your home; and

How to obtain a building permit. This is a very important step to ensure you are rebuilding in compliance with local ordinances.

When your claims adjuster arrives, he/she should show you their official identification (Driver’s License and Company ID or Flood Control Number (FCN card)). The adjuster should also provide you with their contact information, such as their name, email, phone number, the name of their adjusting firm and their telephone number.

What you should expect from your adjuster:

An explanation of the NFIP Flood Claims Process.

An inspection of your property—during which he/she will scope your loss by taking measurements and photos.

An explanation of what an Advance Payment is and how, or if, you can get one.

Information about how you should present your loss to your insurance carrier, and a discussion about your policy coverage.

Other things to know, do and/or discuss with your adjuster:

The insurance carrier, not the adjuster, has the authority to approve your claim.

Be sure to provide your current mailing address and phone number if you are displaced.

The adjuster should never ask you for money or collect your deductible amount.

At the end of your inspection, your adjuster should provide you with information about what you need to do and what will happen next. The adjuster should hand you a physical copy of this information along with his/her contact information. Read more about what to do after your inspection.

Your adjuster may assist you in preparing a Proof of Loss (your sworn statement of the amount you are claiming, including necessary supporting documentation) for your official claim for damage. A Proof of Loss can be many things, but must contain the specific details set forth in the Standard Flood Insurance Policy. You'll need to file your Proof of Loss with your insurance company within 60 days of the date of loss.

You'll receive your claim payment after you and the insurer agree on the amount of damage and the insurer has your complete and signed Proof of Loss. If major catastrophic flooding occurs, it may take longer to process claims.

Note: Signing a Proof of Loss does not waive your rights to file for additional claim payments in the future if additional damage is discovered.

Note: The requirement to file the Proof of Loss could be waived by FEMA depending on the severity of the event. Your adjuster or insurance company will let you know if this happens.

Don't wait until it's too late to get flood insurance!

How Do I Buy Flood Insurance?

National Flood Insurance Program (NFIP) policies can be purchased through thousands of insurance agents nationwide. The agent who helps you with your homeowners or renters insurance may also be able to help you with purchasing flood insurance. Here is a list of participating Write Your Own (WYO) companies.

If your insurance agent does not sell flood insurance, you can contact the NFIP Help Center at 800-427-4661. NFIP flood insurance policies can only be purchased for properties within communities that participate in the NFIP. Ask your agent if your community participates, or look it up online in the Community Status Book.

Why Buy Flood Insurance

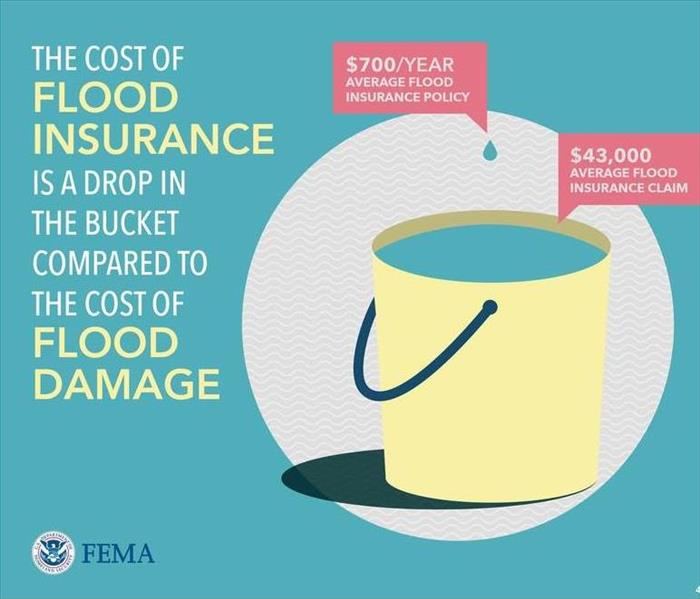

No home is completely safe from potential flooding. Flood insurance can be the difference between recovering and being financially devastated. Just one inch of water in a home can cost more than $25,000 in damage—why risk it?

The Cost of Flooding

Flooding can be an emotionally and financially devastating event. Without flood insurance, most residents have to pay out of pocket or take out loans to repair and replace damaged items. With flood insurance, you're able to recover faster and more fully. Use the tool below to see how much flood damage—even from just a few inches of water—could cost you.

FACT: Flood insurance can pay regardless of whether or not there is a Presidential Disaster Declaration.

FACT: Disaster assistance comes in two forms: a U.S. Small Business Administration loan, which must be paid back with interest, or a FEMA disaster grant, which is about $5,000 on average per household. By comparison, the average flood insurance claim is nearly $30,000 and does not have to be repaid.

All About Flood Maps

The primary feature of flood maps are flood zones, which are geographic areas that FEMA has defined according to varying levels of flood risk and type of flooding. These zones are depicted on the published Flood Insurance Rate Map (FIRM) or Flood Hazard Boundary Map (FHBM). Everyone lives in an area with some risk of flood—it’s just a question of whether you live in a low-, moderate-, or high-risk area.

To find your community’s flood map, visit the FEMA Flood Map Service Center, then type in your address and search. You may view, print and download flood maps, open an interactive flood map (if available), and view all products related to your community.

Find out if your community has pending or preliminary map changes underway. When your community’s flood map is updated to reflect the current risks where you live, requirements for flood insurance coverage and the costs of your policy can also change. Want to receive an alert when your community’s flood map changes? Sign upto receive email notifications when products are updated.

What you pay for flood insurance often has a lot to do with how much flood risk is associated with your building. Mitigation and other factors play a role in protecting properties from flood damage, but sometimes they can also help reduce how much you pay for your flood insurance policy.

Did You Know?

An elevated home, like the one shown in 5 Ways to Lower Your Flood Insurance Premium with a first floor elevated three feet above the Base Flood Elevation (BFE), can expect to save 60% or more on annual flood insurance premiums.

Does my community get a discount?

If your community is enrolled in the Community Rating System (CRS), you may be receiving a discount on your flood insurance. The discount is calculated based on the community's efforts to reduce the risk of flooding. If you have questions about CRS, call your insurance agent or insurer.

Are there ways to protect my property from flood damage?

The Homeowner’s Guide to Retrofitting can help you decide the right method to mitigate future damage and loss by considering various factors, such as hazards to your home, permit requirements, technical limitations and costs. This guide also helps you develop a flood protection strategy.

Elevation: is it the answer?

The Increased Cost of Compliance (ICC) coverage, for eligible properties that are required to be in compliance with local floodplain requirements, can help pay for elevating a building after a flood. Another way to get help with the cost of elevating your building would be through one of FEMA's various grant programs. The grants are administered by states, and each state decides which projects it will fund and for how much. Contact your local floodplain manager for more information.

If you would like to consider elevating your home, learn more about it to determine if it might be a good option. It can be very expensive, but can substantially reduce flood damage and could be a way to reduce the cost of your flood insurance. Here’s another helpful resource: Chapter Five in Homeowner’s Guide to Retrofitting.

The National Flood Insurance Program aims to reduce the impact of flooding on private and public structures.

The National Flood Insurance Program aims to reduce the impact of flooding on private and public structures. It does so by providing affordable insurance to property owners, renters and businesses and by encouraging communities to adopt and enforce floodplain management regulations. These efforts help mitigate the effects of flooding on new and improved structures. Overall, the program reduces the socio-economic impact of disasters by promoting the purchase and retention of general risk insurance, but also of flood insurance, specifically.

This year (2018) the NFIP celebrates 50 years of protecting people in the United States against the perils of flood damage.

HURRICANES HARVEY AND IRMA NOTE: If you've been impacted by Hurricane Harvey, this page provides resources about how to File Your Flood Claim.

I Don't Have Flood Insurance--Why Do I Need It?

Use our interactive tool to find out how much a flood could cost you, and watch this short but informative video to learn more about the value of having flood insurance, Why do I Need to Rethink Insurance?

FACT: Floods are the nation’s most common and costly natural disaster and cause millions of dollars in damage every year.

FACT: Homeowners and renters insurance does not typically cover flood damage.

FACT: Floods can happen anywhere--More than 20 percent of flood claims come from properties outside the high risk flood zone. Check out The Big Cost of Flooding.

FACT: Most federal disaster assistance comes in the form of low-interest disaster loans from U.S. Small Business Administration (SBA) and you have to pay them back. FEMA offers disaster grants that don't need to be paid back, but this amount is often much less than what is needed to recover. A claim against your flood insurance policy could and often does, provide more funds for recovery than those you could qualify for from FEMA or the SBA--and you don't have to pay it back.

FACT:You may be required to have flood insurance. Congress has mandated federally regulated or insured lenders to require flood insurance on mortgaged properties that are located in areas at high risk of flooding. But even if your property is not in a high risk flood area, your mortgage lender may still require you to have flood insurance.

Flood insurance helps more: Check out your state's flood history with FEMA's interactive data visualization tool. Roll your cursor over each county to see how many flooding events have happened. The tool allows you to compare how much FEMA and the U.S. Small Business Administration have provided in terms of federal disaster aid after Presidential Disaster Declarations to the amount the National Flood Insurance program has paid to its policyholders. It's easy to see that having flood insurance provides a lot more help for recovery.

I Have Flood Insurance--Do I Really Need To Keep It?

You realize your flood insurance policy is about to expire and you’re on the fence about renewing: It hasn’t flooded in your area in years (or ever). And you really could use that extra money to buy something you really want. Watch this short, informative video, Why Do I Need to Rethink Insurance?

But wait!

DON’T. RISK. IT.

FACT: Flooding is the most common natural disaster in the United States, affecting every region and state, including yours.

FACT: Flood insurance can be the difference between recovering and being financially devastated.

FACT: The damage from just one inch of water can cost more than $20,000. Check out The Big Cost of Flooding.

FACT:You may be required to have flood insurance. Congress has mandated federally regulated or insured lenders to require flood insurance on mortgaged properties that are located in areas at high risk of flooding. But even if your property is not in a high-risk flood area, your mortgage lender may still require you to have flood insurance.

FACT: If you allow your flood insurance policy to lapse for either more than 90 days, or twice for any number of days, you may be required to provide an Elevation Certificate (if you don't have one), and you may no longer be eligible for policy rate discounts you might have been receiving prior to the policy lapse. It's important to talk with your insurance agent before canceling or not renewing the policy.

FACT: Flood damage is not typically covered by homeowners insurance.

FACT: No home is completely safe from potential flooding devastation—why risk it?

FACT: If you live in a high risk flood zone, and you've received federal disaster assistance in the form of grants from FEMA or low-interest disaster loans from the U.S. Small Business Administration (SBA) following a Presidential Disaster Declaration, you must maintain flood insurance in order to be considered for any future federal disaster aid.

FACT: Storms are not the only cause of floods. Flooding can be caused by dams or levees breaking, new development changing how water flows above and below ground, snowmelt and much more.

FACT: Too often, Americans are caught off guard by the emotional and financial costs of flood damage.

Flood insurance helps more: Check out your state's flood history with FEMA's interactive data Visualization Tool. Roll your cursor over each county to see how many flooding events have happened. The tool allows you to compare how much FEMA has provided in terms of federal disaster aid (through its Individuals & Households Program) after Presidential Disaster Declarations to the amount the National Flood Insurance Program has paid to its policyholders. It's easy to see having flood insurance provides a lot more help for recovery.

To renew your policy, call your flood insurance agent. If you don’t have your insurance agent’s contact information, call the National Flood Insurance Program’s Help Center at 1-800-427-4661.

Who Can Buy Flood Insurance?

If you are a renter or homeowner (residential policy); or business owner (non-residential policy) and your property is located in a NFIP-participating community, you can purchase a policy. Contact your insurance agent to find out if your community participates in the National Flood Insurance Program.

Flood insurance from the NFIP is only available in participating communities. Ask your agent if your state and community participate, or look it up online in the Community Status Book.

Find an insurance agent near you. The agent who helps you with your homeowners or renters insurance may be able to help you with purchasing flood insurance too.

You can only purchase flood insurance through an insurance agent; you cannot buy it directly from the National Flood Insurance Program (NFIP). If your insurance agent does not sell flood insurance, you can:

Contact the National Flood Insurance Program’s Help Center at 1-800-427-4661 to request an agent referral.

How Do I Renew, Change Or Pay For My Flood Insurance Policy?

Your flood insurance agent can help you make changes to, pay for, or renew your flood policy. If your lender requires you to have flood insurance, contact them directly to ask questions about renewing or changing your policy. Your payments could be included in financial transactions associated with your mortgage.

My Question Is About Flood Maps--What Should I Do?

Find out if your community has a recent or upcoming flood map change. When your community’s flood map is updated to reflect the current risks where you live, requirements for flood insurance coverage and the costs of your policy can also change.

Community and state leaders, insurance industry professionals, as well as policyholders, renters, homeowners and businesses will find its resources helpful. We have organized this guide to provide succinct information in an easy-to-navigate document and included important, key contact information. To ensure it can be updated as the program evolves, this document has been published electronically.

Read about everything from mitigating your home to reduce flood damage, to information about weather alerts and how to stay safe when it's flooding in, How to Prepare for a Flood.

Flood claim appeals and guidance (please note--you cannot appeal a claim until you receive a denial [for some or all of your claim amount] from your insurance company.)

What Can I Do To Prepare For Or Even Reduce Flood Damage? And Can Doing These Things Lessen How Much I Pay For Flood Insurance?

What you pay for flood insurance has a lot to do with how much flood risk is associated with your building. It makes sense to reduce flood risk no matter what, but in some instances reducing flood risk can also lead to lower flood insurance costs. Below are some resources to help, but discussing your policy options with your insurance agent is the best place to start.

Communities enrolled in the NFIP's Community Rating System can get discounts on their flood insurance, learn more here.

The Homeowner's Guide to Retrofitting can help you decide the right method to mitigate future damage and loss by considering various factors, such as hazards to your home, permit requirements, technical limitations, and costs. This guide also helps you develop a flood protection strategy.